When it comes to buying a home, one of the first questions that comes to mind is, ‘What is the average mortgage rate? This number has a significant impact on your monthly payments, the total cost of your home, and your long-term financial planning. Understanding mortgage rates is not just about seeing a percentage—it’s about grasping how economic conditions, credit scores, loan types, and market trends all work together to determine what you’ll actually pay.

In this article, we’ll dive deep into what is the average mortgage rate, explore how it’s calculated, discuss influencing factors, provide historical context, and offer tips to help you secure the best possible rate.

What Is the Average Mortgage Rate and Why It Matters

The average mortgage rate represents the typical interest rate lenders charge for a home loan over a specified term, usually 15 or 30 years. It’s calculated based on numerous loans issued across the country, giving prospective homebuyers a benchmark.

Knowing the average mortgage rate is crucial because:

- It directly impacts your monthly mortgage payment.

- A lower rate can save thousands of dollars over the life of the loan.

- It influences affordability and borrowing decisions.

For example, if the average mortgage rate for a 30-year fixed loan is 6%, a $300,000 loan would have a different monthly payment than if the rate were 7%. Even a 0.5% difference in rates can add up to significant extra costs over decades.

Current Average Mortgage Rates in 2026

Mortgage rates fluctuate constantly based on the economy, Federal Reserve policies, inflation, and demand for housing. As of April 2026, here are the latest averages:

| Loan Type | Average Rate | Typical Term |

|---|---|---|

| 30-Year Fixed | 6.25% | 30 years |

| 15-Year Fixed | 5.75% | 15 years |

| 5/1 ARM | 5.95% | Adjustable after 5 years |

Note: These averages reflect national data and can vary based on your state, lender, and credit profile.

Historical Perspective: How Average Mortgage Rates Have Changed

Understanding the historical context can give homebuyers perspective on today’s rates.

| Year | 30-Year Fixed Avg Rate |

|---|---|

| 2000 | 8.05% |

| 2005 | 5.87% |

| 2010 | 4.69% |

| 2015 | 3.85% |

| 2020 | 3.11% |

| 2023 | 6.20% |

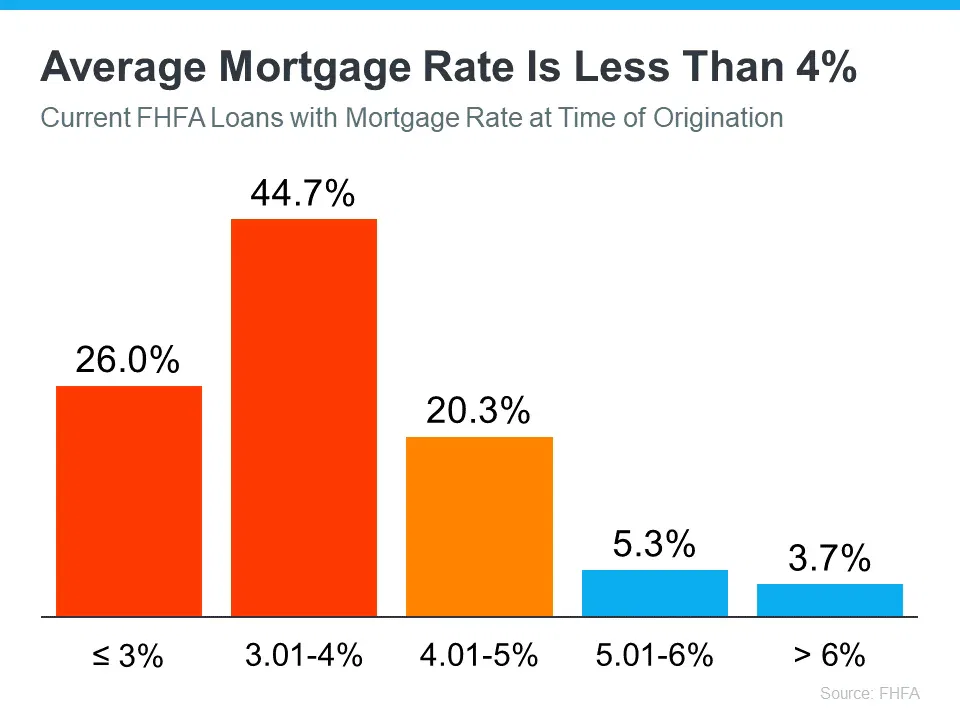

As you can see, mortgage rates have seen significant ups and downs over the past two decades. Homebuyers who locked in low rates in 2020 saved thousands compared to borrowers in 2023.

Factors That Influence the Average Mortgage Rate

Several factors can influence what is the average mortgage rate at any given time:

1. Economic Conditions

Strong economic growth often leads to higher rates as inflation rises and the Federal Reserve adjusts interest rates to maintain balance.

2. Inflation

High inflation reduces the purchasing power of money over time, prompting lenders to increase mortgage rates to maintain returns.

3. Federal Reserve Policy

While the Fed does not set mortgage rates directly, its benchmark interest rates influence long-term rates.

4. Credit Score

Borrowers with excellent credit typically secure rates below the average, while lower credit scores can result in higher rates.

5. Loan Type

Fixed-rate loans usually have higher rates than adjustable-rate mortgages (ARMs) initially, but ARMs can change over time.

6. Loan Term

Shorter-term loans (15 years) tend to have lower average rates than 30-year loans due to lower risk for lenders.

How to Calculate Your Monthly Payment Using Average Rates

The average mortgage rate is just the starting point. To understand your payment, you need to include principal, interest, taxes, and insurance (PITI).

For example, consider a $300,000 home loan at the current 30-year average mortgage rate of 6.25%:

| Loan Amount | Rate | Term | Monthly Principal & Interest |

|---|---|---|---|

| $300,000 | 6.25% | 30 years | $1,845 |

Taxes and insurance may add $300–$500 depending on your location.

Tip: Even small reductions in rates can make a significant difference. Dropping from 6.25% to 5.75% saves roughly $150 per month.

Differences Between Fixed and Adjustable Rates

- Fixed-Rate Mortgages: Your interest rate remains the same for the life of the loan, offering predictability.

- Adjustable-Rate Mortgages (ARMs): Start with a lower rate but adjust periodically based on market conditions. The average mortgage rate for a 5/1 ARM is slightly lower than a 30-year fixed rate but can increase after the initial period.

Tips for Securing the Best Average Rate

- Check Your Credit Score: The higher your score, the closer you can get to below-average rates.

- Shop Around: Different lenders offer slightly different rates. A small difference can save thousands.

- Consider Points: Paying points upfront can lower your average mortgage rate over time.

- Timing Matters: Mortgage rates fluctuate daily. Even a week’s difference can impact your rate.

- Evaluate Loan Types: If you plan to sell or refinance within a few years, an ARM might save money despite higher long-term rates.

Average Rates by State

Mortgage rates can also vary by state due to local economic conditions and lender competition. Here is a snapshot:

| State | Average 30-Year Fixed Rate |

|---|---|

| California | 6.10% |

| Texas | 6.35% |

| New York | 6.20% |

| Florida | 6.25% |

| Illinois | 6.30% |

Local differences are generally within a 0.2–0.3% range of the national average.

Refinancing and Average Rates

Refinancing allows homeowners to replace an existing mortgage with a new loan at a lower rate. When the national average mortgage rate drops, refinancing becomes an attractive option:

- Example: A homeowner with a $250,000 loan at 6.5% might refinance to 5.75%, reducing monthly payments by $100–$150.

- Keep in mind closing costs and fees may offset immediate savings.

Factors to Watch in 2026

Experts anticipate several trends influencing what is the average mortgage rate:

- Federal Reserve may adjust interest rates depending on inflation trends.

- Housing demand could push rates higher if supply remains constrained.

- Economic growth or slowdown can impact lenders’ risk assessments.

- Credit quality requirements may tighten slightly, affecting average rates for some borrowers.

FAQs on What Is the Average Mortgage Rate

Q1: What is the current average mortgage rate?

A1: As of April 2026, the 30-year fixed average mortgage rate is approximately 6.25%.

Q2: Does the average mortgage rate include fees?

A2: No, the average rate reflects interest only. Closing costs, taxes, and insurance are additional.

Q3: How often do mortgage rates change?

A3: Mortgage rates can change daily based on market conditions, lender decisions, and economic data.

Q4: Can I get a rate below the average mortgage rate?

A4: Yes, borrowers with high credit scores and strong financials often secure below-average rates.

Q5: What is better, a fixed or adjustable rate?

A5: It depends on your plans. Fixed offers stability; adjustable can start lower but may increase over time.

Q6: How do I track changes in average mortgage rates?

A6: Use financial news outlets, lender websites, or government housing data to monitor national averages.

Q7: How much does my credit score impact the rate?

A7: A high credit score (750+) can lower your rate by 0.5–1% compared to someone with a score below 650.

Conclusion

Understanding what is the average mortgage rate is vital for any prospective homebuyer or homeowner considering refinancing. Rates affect monthly payments, overall loan costs, and financial planning. By staying informed, comparing offers, and considering your unique financial situation, you can make smarter decisions and potentially save tens of thousands over the life of your loan.

Whether you’re buying your first home, upgrading, or refinancing, knowing the average mortgage rate—and the factors that influence it—empowers you to make the best choice for your future.